This is an excerpt from the 0xResearch newsletter. To read full editions, subscribe.

In an open-source industry where applications can and do easily fork, “aggregation theory”—the investor thesis that the winner should build on and integrate as many applications as possible—has emerged as a promising idea during the DeFi summer.

DeFi middleware aggregators such as 1inch, Matcha, Summer.fi (formerly Oasis) and Instadapp have implemented this idea to its fullest, but the aggregation theory has largely fallen short (Jupiter in the Solana world is an exception).

Ethereum DEX aggregators have not surpassed Uniswap, although in theory they should.

Instadapp was one such DeFi aggregator that was actively building on top of DeFi protocols such as Uniswap, Maker, Aave, Compound, and Curve.

After two years of development, Instadapp has reinvented itself. From being the creator of a classic aggregator product, Instadapp has evolved into a platform with a full-fledged DeFi product: Fluid, while the original Instadapp app exists separately as a yield aggregator product.

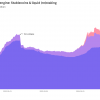

Instadapp’s pivot has been quite successful: Fluid currently has $1.2 billion in TVL on its money market, while the Fluid DEX on Ethereum has around $428 million in 7-day trading volumes – currently the third largest DEX after Curve and Uniswap.

Let’s go back a minute. What is liquid?

The first thing you need to know is that Fluid is not one app, but an ecosystem of super apps. Fluid’s pooled liquidity layer forms the backbone of the protocol, on top of which sits its own DEX (launched in early November), money market, and other storage applications.

The Fluid suite of apps heavily borrows many market-proven DeFi primitives such as Uni v1 auto-rebalancing, Uni v3 concentrated liquidity, Aave utilization curves, Maker Vault debt ceilings, and more.

But it also offers many of DeFi’s original innovations, namely more capital-efficient ways to provide liquidity, thanks to its smart collateral and smart debt features.

For example, smart debt allows borrowers to denominate their debt into trading pairs as liquidity for the Fluid DEX trading pool.

Thus, Fluid DEX traders can trade assets against other people’s debts. From a borrower’s perspective, you can maintain active credit while earning commissions from traders to pay off your original debt, thereby turning debt into a productive asset.

In general, smart debt creates liquidity in the exact opposite direction whereby LPs contribute liquidity to the AMM pool (i.e. contribute liquidity to two tokens and receive an LP token).

Smart Debt has allowed trading pools like USDC-USDT with $20 million in liquidity to appear on the Fluid DEX even though they are technically worth $0 in TVL.

Smart Collateral, on the other hand, allows LPs to take their LP positions out of lending and re-pledge them as collateral for AMM liquidity on the Fluid DEX. This allows LPs to earn commissions for DEX trading on top of lending fees.

This isn’t technically new—in the past, DEXs like Cream Finance have experimented with the ability to use LP tokens as collateral—but Fluid manages to implement it more efficiently.

“With Fluid DEX v2, we plan to give users the ability to select ranges by both collateral and debt, which will be a breakthrough,” Instadapp DMH COO told Blockworks.

Fluid governance is governed by the INST token. The token historically remained dead until it was 4xed last month.

The new management proposal released yesterday aims to convert INST to FLUID at a 1:1 ratio without any dilution or change in the overall supply.

Upon reaching the $10 million annual revenue goal, Fluid will begin a token buyback program to increase the value of the token.

Finally, the proposal also proposes spending 12% of tokens to fund growth initiatives such as CEX listings, market creation and fundraising, as well as staking an additional 5% of tokens for FLUID liquidity on DEXs.